Page 117 - Microsoft Word - 00 CIMA F1 Prelims STUDENT 2018.docx

P. 117

Internal audit

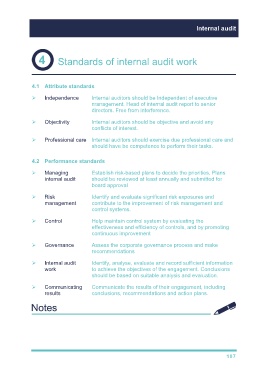

Standards of internal audit work

4.1 Attribute standards

Independence Internal auditors should be Independent of executive

management. Head of internal audit report to senior

directors. Free from interference.

Objectivity Internal auditors should be objective and avoid any

conflicts of interest.

Professional care Internal auditors should exercise due professional care and

should have be competence to perform their tasks.

4.2 Performance standards

Managing Establish risk-based plans to decide the priorities. Plans

internal audit should be reviewed at least annually and submitted for

board approval

Risk Identify and evaluate significant risk exposures and

management contribute to the improvement of risk management and

control systems.

Control Help maintain control system by evaluating the

effectiveness and efficiency of controls, and by promoting

continuous improvement

Governance Assess the corporate governance process and make

recommendations

Internal audit Identify, analyse, evaluate and record sufficient information

work to achieve the objectives of the engagement. Conclusions

should be based on suitable analysis and evaluation.

Communicating Communicate the results of their engagement, including

results conclusions, recommendations and action plans.

107