Page 119 - Microsoft Word - 00 CIMA F1 Prelims STUDENT 2018.docx

P. 119

Internal audit

Internal and external audit

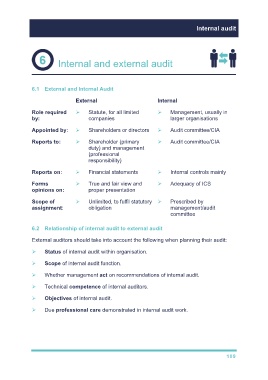

6.1 External and Internal Audit

Role required Statute, for all limited Management, usually in

by: companies larger organisations

Appointed by: Shareholders or directors Audit committee/CIA

Reports to: Shareholder (primary Audit committee/CIA

duty) and management

(professional

responsibility)

Reports on: Financial statements Internal controls mainly

Forms True and fair view and Adequacy of ICS

opinions on: proper presentation

Scope of Unlimited, to fulfil statutory Prescribed by

assignment: obligation management/audit

committee

6.2 Relationship of internal audit to external audit

External auditors should take into account the following when planning their audit:

Status of internal audit within organisation.

Scope of internal audit function.

Whether management act on recommendations of internal audit.

Technical competence of internal auditors.

Objectives of internal audit.

Due professional care demonstrated in internal audit work.

109