Page 14 - PowerPoint Presentation

P. 14

DECISION MAKING

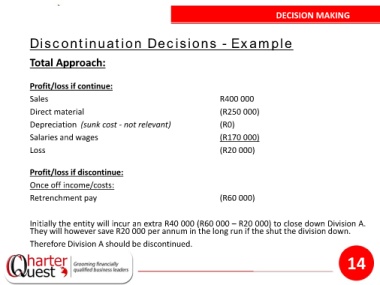

Discontinuation Decisions - Example

Total Approach:

Profit/loss if continue:

Sales R400 000

Direct material (R250 000)

Depreciation (sunk cost - not relevant) (R0)

Salaries and wages (R170 000)

Loss (R20 000)

Profit/loss if discontinue:

Once off income/costs:

Retrenchment pay (R60 000)

Initially the entity will incur an extra R40 000 (R60 000 – R20 000) to close down Division A.

They will however save R20 000 per annum in the long run if the shut the division down.

Therefore Division A should be discontinued.

14