Page 18 - PowerPoint Presentation

P. 18

DECISION MAKING

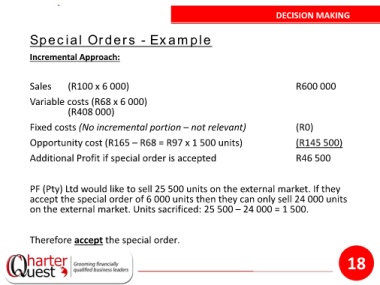

Special Orders - Example

Incremental Approach:

Sales (R100 x 6 000) R600 000

Variable costs (R68 x 6 000)

(R408 000)

Fixed costs (No incremental portion – not relevant) (R0)

Opportunity cost (R165 – R68 = R97 x 1 500 units) (R145 500)

Additional Profit if special order is accepted R46 500

PF (Pty) Ltd would like to sell 25 500 units on the external market. If they

accept the special order of 6 000 units then they can only sell 24 000 units

on the external market. Units sacrificed: 25 500 – 24 000 = 1 500.

Therefore accept the special order.

18