Page 35 - BA2 Integrated Workbook - Student 2017

P. 35

Cost identification and classification

3.3 Semi-variable cost

The CIMA Terminology defines a semi-variable cost as a ‘cost

containing both fixed and variable components and thus partly affected

by a change in the level of activity’.

Examples of semi-variable costs:

Electricity

Telephone

Photocopier

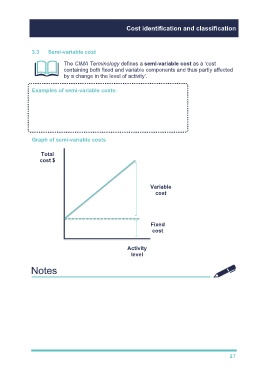

Graph of semi-variable costs

Total

cost $

Variable

cost

Fixed

cost

Activity

level

TYU 4

27