Page 336 - SBR Integrated Workbook STUDENT S18-J19

P. 336

Chapter 21

3.2 Changes in group structure

Acquisition of a subsidiary

In the consolidated statement of cash flows the entity must record the actual cash

flow for the purchase of the subsidiary net of any cash held by the subsidiary that is

now controlled by the group.

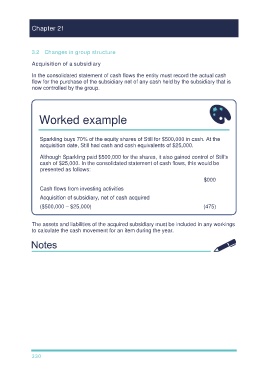

Worked example

Sparkling buys 70% of the equity shares of Still for $500,000 in cash. At the

acquisition date, Still had cash and cash equivalents of $25,000.

Although Sparkling paid $500,000 for the shares, it also gained control of Still's

cash of $25,000. In the consolidated statement of cash flows, this would be

presented as follows:

$000

Cash flows from investing activities

Acquisition of subsidiary, net of cash acquired

($500,000 – $25,000) (475)

The assets and liabilities of the acquired subsidiary must be included in any workings

to calculate the cash movement for an item during the year.

330