Page 471 - SBR Integrated Workbook STUDENT S18-J19

P. 471

Answers

Example 9 – continued

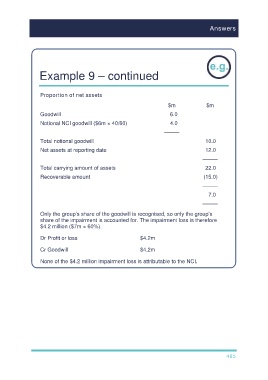

Proportion of net assets

$m $m

Goodwill 6.0

Notional NCI goodwill ($6m × 40/60) 4.0

–––––

Total notional goodwill 10.0

Net assets at reporting date 12.0

–––––

Total carrying amount of assets 22.0

Recoverable amount (15.0)

–––––

7.0

–––––

Only the group’s share of the goodwill is recognised, so only the group’s

share of the impairment is accounted for. The impairment loss is therefore

$4.2 million ($7m × 60%).

Dr Profit or loss $4.2m

Cr Goodwill $4.2m

None of the $4.2 million impairment loss is attributable to the NCI.

465