Page 476 - SBR Integrated Workbook STUDENT S18-J19

P. 476

Chapter 25

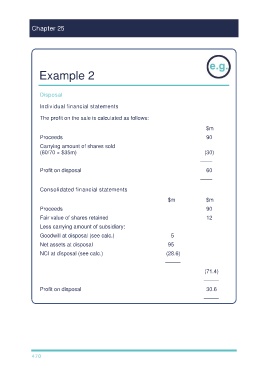

Example 2

Disposal

Individual financial statements

The profit on the sale is calculated as follows:

$m

Proceeds 90

Carrying amount of shares sold

(60/70 × $35m) (30)

––––

Profit on disposal 60

––––

Consolidated financial statements

$m $m

Proceeds 90

Fair value of shares retained 12

Less carrying amount of subsidiary:

Goodwill at disposal (see calc.) 5

Net assets at disposal 95

NCI at disposal (see calc.) (28.6)

–––––

(71.4)

–––––

Profit on disposal 30.6

–––––

470