Page 65 - SBR Integrated Workbook STUDENT S18-J19

P. 65

Non-current assets

Property, plant and equipment

1.1 Definitions

IAS 16 Property, Plant and Equipment (PPE) defines PPE as tangible

items which are used to produce or supply goods, for rental, or for

administrative purposes over more than one period.

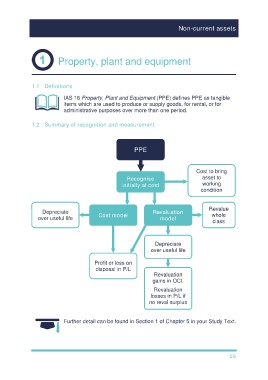

1.2 Summary of recognition and measurement

PPE

Cost to bring

Recognise asset to

initially at cost working

condition

Revalue

Depreciate Revaluation whole

over useful life Cost model model

class

Depreciate

over useful life

Profit or loss on

disposal in P/L

Revaluation

gains in OCI.

Revaluation

losses in P/L if

no reval surplus

Further detail can be found in Section 1 of Chapter 5 in your Study Text.

59