Page 67 - SBR Integrated Workbook STUDENT S18-J19

P. 67

Non-current assets

Government grants

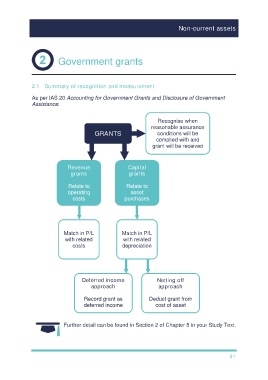

2.1 Summary of recognition and measurement

As per IAS 20 Accounting for Government Grants and Disclosure of Government

Assistance:

Recognise when

reasonable assurance

GRANTS conditions will be

complied with and

grant will be received

Revenue Capital

grants grants

Relate to Relate to

operating asset

costs purchases

Match in P/L Match in P/L

with related with related

costs depreciation

Deferred income Netting off

approach approach

Record grant as Deduct grant from

deferred income cost of asset

Further detail can be found in Section 2 of Chapter 5 in your Study Text.

61