Page 117 - Microsoft Word - 00 IWB ACCA F7.docx

P. 117

Systems and controls

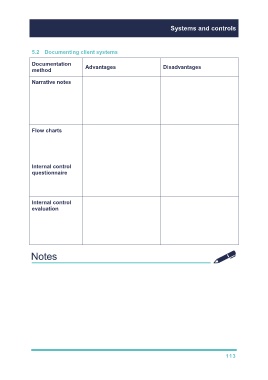

5.2 Documenting client systems

Documentation

method Advantages Disadvantages

Narrative notes Simple to record Time consuming to

prepare and

Facilitate understanding cumbersome if system is

by all audit staff complex

Difficult to identify

missing controls

Flow charts Easy to view the whole Still a need for narrative

system notes

Easy to spot missing Difficult to amend

controls

Internal control Quick to prepare Controls may be

questionnaire overstated

Can ensure all controls

are present Unusual controls unlikely

to be included

Internal control Controls less likely to be Checklist may contain

evaluation overstated control objectives not

relevant to the client

Quick to prepare

Unusual risks and

control objectives may

not be identified

113