Page 6 - AB INBEV MODEL ANSWER 1

P. 6

P a ge | 6

not be addressed, we envisage that we would have spent, instead of the BAC of US$290 million, EAC

of US$1billion (3.5 times higher –an overrun of US$710 million, before taking into account time value

of money)!

Appendix 3.2 Cost-synergies: Over the 4 years, we envisage the cost synergies to total US$9,800

million (BAC) (from cost and revenue synergies of US$2,660 per annum as provided in the scenario,

of which 92% is cost synergies of US$2450million), and based on the plan to have extracted 50% of

these cost synergies by the mind-way point (October 3, 2018), total savings are expected to be

US$1,486million (BCWS), but our forecasted performance show we would have only realized

US$772million (BCWP) in cost synergies (shortfall of US$714million).

Where is the challenge? Our integration plan is designed to re-engineer our combined cost structures

and release synergies around four key activities (A, B, C and D) as extracted and tabled from Appendix

3.1 and 3.2 below:

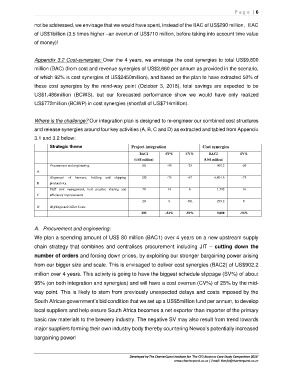

Strategic theme Project integration Cost synergies

BAC1 SV% CV% BAC2 SV%

(US$ million) (US$ million)

Procurement and engineering. 80 -95 -25 907.2 -95

A

Alignment of brewery, bottling and shipping 120 -75 -67 6,801.6 -75

B productivity.

Staff cost management, best practice sharing and 70 14 6 1,792 14

C efficiency improvements

20 0 -381 299.2 0

D HQ/Regional Office Costs

290 -54% -59% 9,800 -54%

A. Procurement and engineering:

We plan a spending amount of US$ 80 million (BAC1) over 4 years on a new upstream supply

chain strategy that combines and centralises procurement including JIT – cutting down the

number of orders and forcing down prices, by exploiting our stronger bargaining power arising

from our bigger size and scale. This is envisaged to deliver cost synergies (BAC2) of US$902.2

million over 4 years. This activity is going to have the biggest schedule slippage (SV%) of about

95% (on both integration and synergies) and will have a cost overrun (CV%) of 25% by the mid-

way point. This is likely to stem from previously unexpected delays and costs imposed by the

South African government’s bid condition that we set up a US$5million fund per annum, to develop

local suppliers and help ensure South Africa becomes a net exporter than importer of the primary

basic raw materials to the brewery industry. The negative SV may also result from trend towards

major suppliers forming their own industry body thereby countering Newco’s potentially increased

bargaining power!

Developed by The CharterQuest Institute for 'The CFO Business Case Study Competition 2018'

www.charterquest.co.za | Email: thecfo@charterquest.co.za