Page 247 - Microsoft Word - 00 P1 IW Prelims.docx

P. 247

Complex groups

Example 2

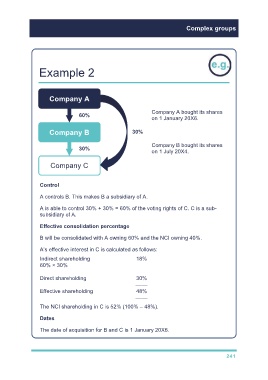

Company A

Company A bought its shares

60%

on 1 January 20X6.

Company B 30%

Company B bought its shares

30% on 1 July 20X4.

Company C

Control

A controls B. This makes B a subsidiary of A.

A is able to control 30% + 30% = 60% of the voting rights of C. C is a sub-

subsidiary of A.

Effective consolidation percentage

B will be consolidated with A owning 60% and the NCI owning 40%.

A’s effective interest in C is calculated as follows:

Indirect shareholding 18%

60% × 30%

Direct shareholding 30%

––––

Effective shareholding 48%

––––

The NCI shareholding in C is 52% (100% – 48%).

Dates

The date of acquisition for B and C is 1 January 20X6.

241