Page 117 - Microsoft Word - 00 IWB ACCA F7.docx

P. 117

Financial assets and financial liabilities

Example 1

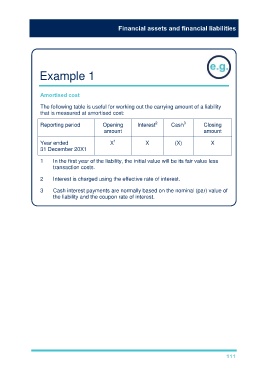

Amortised cost

The following table is useful for working out the carrying amount of a liability

that is measured at amortised cost:

Reporting period Opening Interest 2 Cash 3 Closing

amount amount

Year ended X 1 X (X) X

31 December 20X1

1 In the first year of the liability, the initial value will be its fair value less

transaction costs.

2 Interest is charged using the effective rate of interest.

3 Cash interest payments are normally based on the nominal (par) value of

the liability and the coupon rate of interest.

111