Page 240 - Microsoft Word - 00 CIMA F1 Prelims STUDENT 2018.docx

P. 240

Chapter 12

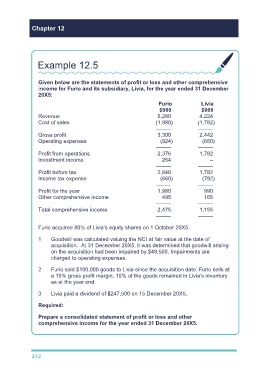

Example 12.5

Given below are the statements of profit or loss and other comprehensive

income for Furio and its subsidiary, Livia, for the year ended 31 December

20X5:

Furio Livia

$000 $000

Revenue 5,280 4,224

Cost of sales (1,980) (1,782)

––––– –––––

Gross profit 3,300 2,442

Operating expenses (924) (660)

––––– –––––

Profit from operations 2,376 1,782

Investment income 264 –

––––– –––––

Profit before tax 2,640 1,782

Income tax expense (660) (792)

––––– –––––

Profit for the year 1,980 990

Other comprehensive income 495 165

––––– –––––

Total comprehensive income 2,475 1,155

––––– –––––

Furio acquired 80% of Livia’s equity shares on 1 October 20X5.

1 Goodwill was calculated valuing the NCI at fair value at the date of

acquisition. At 31 December 20X5, it was determined that goodwill arising

on the acquisition had been impaired by $49,500. Impairments are

charged to operating expenses.

2 Furio sold $100,000 goods to Livia since the acquisition date. Furio sells at

a 10% gross profit margin. 10% of the goods remained in Livia’s inventory

as at the year end.

3 Livia paid a dividend of $247,500 on 15 December 20X5.

Required:

Prepare a consolidated statement of profit or loss and other

comprehensive income for the year ended 31 December 20X5.

232