Page 317 - Microsoft Word - 00 CIMA F1 Prelims STUDENT 2018.docx

P. 317

Consolidated statement of changes in equity

2.2 Impacts of transfer between owners (control to control) on CSOCIE

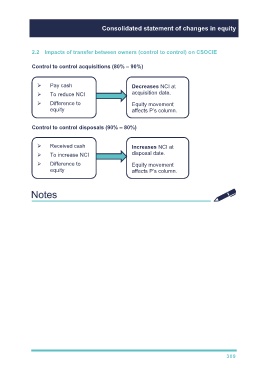

Control to control acquisitions (80% – 90%)

Pay cash Decreases NCI at

To reduce NCI acquisition date.

Difference to Equity movement

equity affects P’s column.

Control to control disposals (90% – 80%)

Received cash Increases NCI at

To increase NCI disposal date.

Difference to Equity movement

equity affects P’s column.

309