Page 121 - BA2 Integrated Workbook STUDENT 2018

P. 121

Budgeting

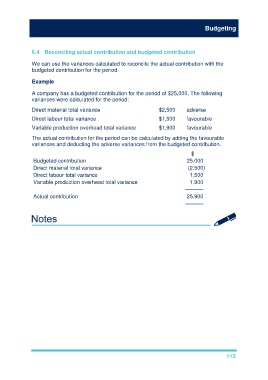

6.4 Reconciling actual contribution and budgeted contribution

We can use the variances calculated to reconcile the actual contribution with the

budgeted contribution for the period.

Example

A company has a budgeted contribution for the period of $25,000. The following

variances were calculated for the period:

Direct material total variance $2,500 adverse

Direct labour total variance $1,500 favourable

Variable production overhead total variance $1,900 favourable

The actual contribution for the period can be calculated by adding the favourable

variances and deducting the adverse variances from the budgeted contribution.

$

Budgeted contribution 25,000

Direct material total variance (2,500)

Direct labour total variance 1,500

Variable production overhead total variance 1,900

––––––

Actual contribution 25,900

––––––

115