Page 150 - BA2 Integrated Workbook STUDENT 2018

P. 150

Chapter 8

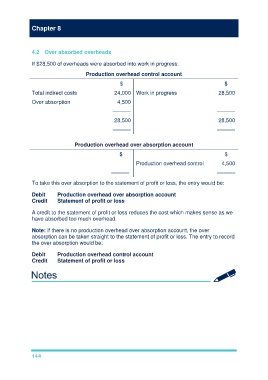

4.2 Over absorbed overheads

If $28,500 of overheads were absorbed into work in progress:

Production overhead control account

$ $

Total indirect costs 24,000 Work in progress 28,500

Over absorption 4,500

–––––– ––––––

28,500 28,500

–––––– ––––––

Production overhead over absorption account

$ $

Production overhead control 4,500

–––––– ––––––

To take this over absorption to the statement of profit or loss, the entry would be:

Debit Production overhead over absorption account

Credit Statement of profit or loss

A credit to the statement of profit or loss reduces the cost which makes sense as we

have absorbed too much overhead.

Note: If there is no production overhead over absorption account, the over

absorption can be taken straight to the statement of profit or loss. The entry to record

the over absorption would be:

Debit Production overhead control account

Credit Statement of profit or loss

144