Page 65 - BA2 Integrated Workbook STUDENT 2018

P. 65

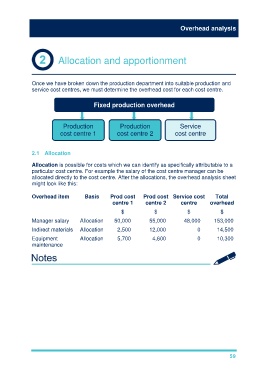

Overhead analysis

Allocation and apportionment

Once we have broken down the production department into suitable production and

service cost centres, we must determine the overhead cost for each cost centre.

Fixed production overhead

Production Production Service

cost centre 1 cost centre 2 cost centre

2.1 Allocation

Allocation is possible for costs which we can identify as specifically attributable to a

particular cost centre. For example the salary of the cost centre manager can be

allocated directly to the cost centre. After the allocations, the overhead analysis sheet

might look like this:

Overhead item Basis Prod cost Prod cost Service cost Total

centre 1 centre 2 centre overhead

$ $ $ $

Manager salary Allocation 50,000 55,000 48,000 153,000

Indirect materials Allocation 2,500 12,000 0 14,500

Equipment Allocation 5,700 4,600 0 10,300

maintenance

59