Page 70 - BA2 Integrated Workbook STUDENT 2018

P. 70

Chapter 4

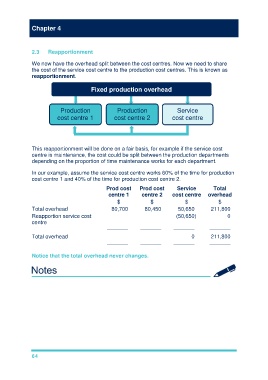

2.3 Reapportionment

We now have the overhead split between the cost centres. Now we need to share

the cost of the service cost centre to the production cost centres. This is known as

reapportionment.

Fixed production overhead

Production Production Service

cost centre 1 cost centre 2 cost centre

This reapportionment will be done on a fair basis, for example if the service cost

centre is maintenance, the cost could be split between the production departments

depending on the proportion of time maintenance works for each department.

In our example, assume the service cost centre works 60% of the time for production

cost centre 1 and 40% of the time for production cost centre 2.

Prod cost Prod cost Service Total

centre 1 centre 2 cost centre overhead

$ $ $ $

Total overhead 80,700 80,450 50,650 211,800

Reapportion service cost 30,390 20,260 (50,650) 0

centre

––––––– ––––––– ––––––– –––––––

Total overhead 111,090 100,710 0 211,800

––––––– ––––––– ––––––– –––––––

Notice that the total overhead never changes.

64