Page 8 - PowerPoint Presentation

P. 8

VARIABLE AND ABSORPTION COSTING

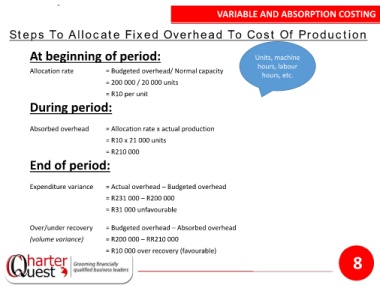

Steps To Allocate Fixed Overhead To Cost Of Production

At beginning of period: Units, machine

hours, labour

Allocation rate = Budgeted overhead/ Normal capacity hours, etc.

= 200 000 / 20 000 units

= R10 per unit

During period:

Absorbed overhead = Allocation rate x actual production

= R10 x 21 000 units

= R210 000

End of period:

Expenditure variance = Actual overhead – Budgeted overhead

= R231 000 – R200 000

= R31 000 unfavourable

Over/under recovery = Budgeted overhead – Absorbed overhead

(volume variance) = R200 000 – RR210 000

= R10 000 over recovery (favourable)

8