Page 207 - Microsoft Word - 00 - Prelims.docx

P. 207

Statement of cash flows

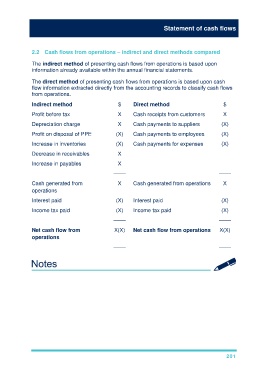

2.2 Cash flows from operations – indirect and direct methods compared

The indirect method of presenting cash flows from operations is based upon

information already available within the annual financial statements.

The direct method of presenting cash flows from operations is based upon cash

flow information extracted directly from the accounting records to classify cash flows

from operations.

Indirect method $ Direct method $

Profit before tax X Cash receipts from customers X

Depreciation charge X Cash payments to suppliers (X)

Profit on disposal of PPE (X) Cash payments to employees (X)

Increase in inventories (X) Cash payments for expenses (X)

Decrease in receivables X

Increase in payables X

–––– ––––

Cash generated from X Cash generated from operations X

operations

Interest paid (X) Interest paid (X)

Income tax paid (X) Income tax paid (X)

–––– ––––

Net cash flow from X(X) Net cash flow from operations X(X)

operations

–––– ––––

201