Page 259 - Microsoft Word - 00 - Prelims.docx

P. 259

Consolidated financial statements II

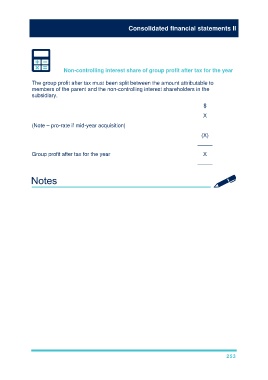

Non-controlling interest share of group profit after tax for the year

The group profit after tax must been split between the amount attributable to

members of the parent and the non-controlling interest shareholders in the

subsidiary.

$

NCI % of subsidiary profit after tax for the year X

(Note – pro-rate if mid-year acquisition)

(X)

–––––

Group profit after tax for the year X

–––––

253