Page 261 - Microsoft Word - 00 - Prelims.docx

P. 261

Consolidated financial statements II

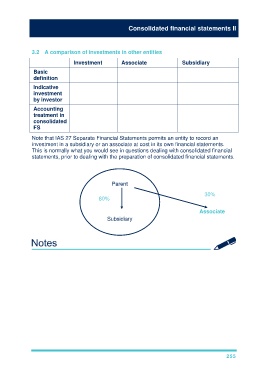

3.2 A comparison of investments in other entities

Investment Associate Subsidiary

Basic Neither influence Influence Control

definition nor control

Indicative Less than 20% Between 20% and In excess of 50%

investment 50%

by investor

Accounting Usually measure Equity method of Consolidation

treatment in at either cost or accounting

consolidated fair value

FS

Note that IAS 27 Separate Financial Statements permits an entity to record an

investment in a subsidiary or an associate at cost in its own financial statements.

This is normally what you would see in questions dealing with consolidated financial

statements, prior to dealing with the preparation of consolidated financial statements.

Parent

30%

80%

Associate

Subsidiary

255