Page 140 - F2 - MA Integrated Workbook STUDENT 2018-19

P. 140

Chapter 7

Allocation and apportionment

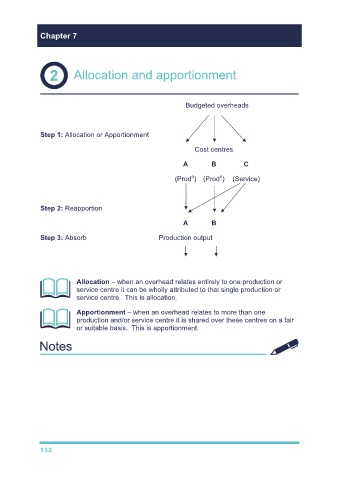

Budgeted overheads

Step 1: Allocation or Apportionment

Cost centres

A B C

n

n

(Prod ) (Prod ) (Service)

Step 2: Reapportion

A B

Step 3: Absorb Production output

Allocation – when an overhead relates entirely to one production or

service centre it can be wholly attributed to that single production or

service centre. This is allocation.

Apportionment – when an overhead relates to more than one

production and/or service centre it is shared over these centres on a fair

or suitable basis. This is apportionment.

132