Page 151 - F2 - MA Integrated Workbook STUDENT 2018-19

P. 151

Accounting for overheads

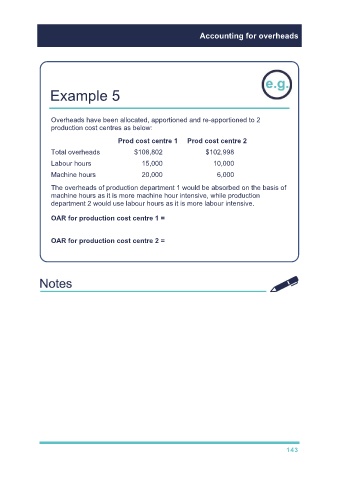

Example 5

Overheads have been allocated, apportioned and re-apportioned to 2

production cost centres as below:

Prod cost centre 1 Prod cost centre 2

Total overheads $108,802 $102,998

Labour hours 15,000 10,000

Machine hours 20,000 6,000

The overheads of production department 1 would be absorbed on the basis of

machine hours as it is more machine hour intensive, while production

department 2 would use labour hours as it is more labour intensive.

OAR for production cost centre 1 = $108,802 ÷ 20,000 = $5.44 per

machine hour

OAR for production cost centre 2 = $102,998 ÷ 10,000 = $10.30 per labour

hour

143