Page 406 - F2 - MA Integrated Workbook STUDENT 2018-19

P. 406

Chapter 15

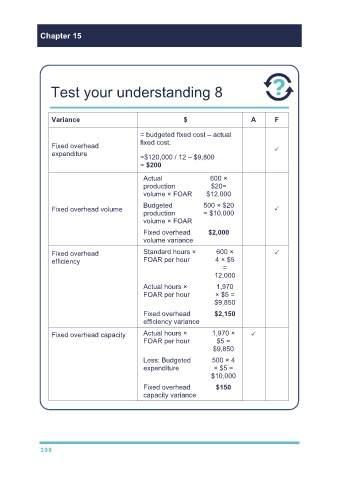

Test your understanding 8

Variance $ A F

= budgeted fixed cost – actual

fixed cost.

Fixed overhead

expenditure

=$120,000 / 12 – $9,800

= $200

Actual 600 ×

production $20=

volume × FOAR $12,000

Budgeted 500 × $20

Fixed overhead volume

production = $10,000

volume × FOAR

Fixed overhead $2,000

volume variance

Fixed overhead Standard hours × 600 ×

efficiency FOAR per hour 4 × $5

=

12,000

Actual hours × 1,970

FOAR per hour × $5 =

$9,850

Fixed overhead $2,150

efficiency variance

Fixed overhead capacity Actual hours × 1,970 ×

FOAR per hour $5 =

$9,850

Less: Budgeted 500 × 4

expenditure × $5 =

$10,000

Fixed overhead $150

capacity variance

398