Page 474 - F2 - MA Integrated Workbook STUDENT 2018-19

P. 474

Chapter 18

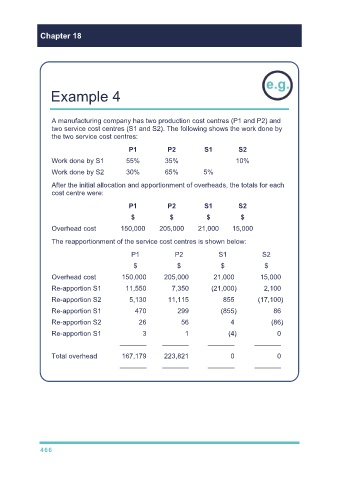

Example 4

A manufacturing company has two production cost centres (P1 and P2) and

two service cost centres (S1 and S2). The following shows the work done by

the two service cost centres:

P1 P2 S1 S2

Work done by S1 55% 35% 10%

Work done by S2 30% 65% 5%

After the initial allocation and apportionment of overheads, the totals for each

cost centre were:

P1 P2 S1 S2

$ $ $ $

Overhead cost 150,000 205,000 21,000 15,000

The reapportionment of the service cost centres is shown below:

P1 P2 S1 S2

$ $ $ $

Overhead cost 150,000 205,000 21,000 15,000

Re-apportion S1 11,550 7,350 (21,000) 2,100

Re-apportion S2 5,130 11,115 855 (17,100)

Re-apportion S1 470 299 (855) 86

Re-apportion S2 26 56 4 (86)

Re-apportion S1 3 1 (4) 0

––––––– ––––––– ––––––– –––––––

Total overhead 167,179 223,821 0 0

––––––– ––––––– ––––––– –––––––

466