Page 100 - Microsoft Word - 00 ACCA F2 Prelims.docx

P. 100

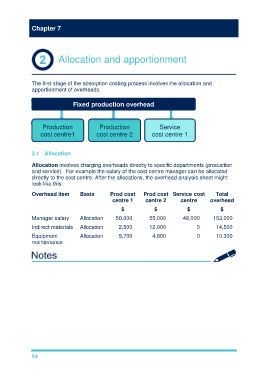

Chaptter 7

Alloocationn and apportionmment

The firsst stage of the absorpption costinng processs involves the allocattion and

apportionment of f overheadss.

Fixed prroductionn overheead

Prroduction Producttion Servvice

cosst centre11 cost centtre 2 cost ceentre 1

2.1 AAllocation

Allocattion involvves charginng overheaads directlyy to specific departmeents (production

and service). Forr example the salary of the cosst centre manager caan be allocaated

directlyy to the cosst centre. AAfter the allocations, the overheead analyssis sheet mmight

look likke this:

Overheead item Basis Prodd cost P Prod cost Service cost T Total

cenntre 1 centre 2 centrre oveerhead

$ $ $ $

Manager salary Allocatiion 500,000 55,000 48,000 1553,000

Indirectt materialss Allocatiion 22,500 12,000 0 1 14,500

Equipmment Allocatiion 55,700 4,600 0 1 10,300

maintenance

94