Page 108 - Microsoft Word - 00 ACCA F2 Prelims.docx

P. 108

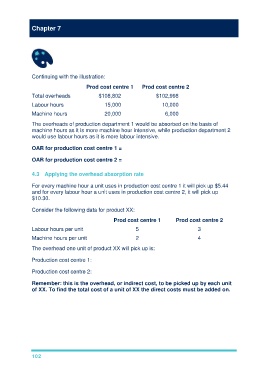

Chapter 7

Continuing with the illustration:

Prod cost centre 1 Prod cost centre 2

Total overheads $108,802 $102,998

Labour hours 15,000 10,000

Machine hours 20,000 6,000

The overheads of production department 1 would be absorbed on the basis of

machine hours as it is more machine hour intensive, while production department 2

would use labour hours as it is more labour intensive.

OAR for production cost centre 1 = $108,802 ÷ 20,000 = $5.44 per machine hour

OAR for production cost centre 2 = $102,998 ÷ 10,000 = $10.30 per labour hour

4.3 Applying the overhead absorption rate

For every machine hour a unit uses in production cost centre 1 it will pick up $5.44

and for every labour hour a unit uses in production cost centre 2, it will pick up

$10.30.

Consider the following data for product XX:

Prod cost centre 1 Prod cost centre 2

Labour hours per unit 5 3

Machine hours per unit 2 4

The overhead one unit of product XX will pick up is:

Production cost centre 1: 2 machine hours × $5.44 = $10.88

Production cost centre 2: 3 labour hours × $10.30 = $30.90

Remember: this is the overhead, or indirect cost, to be picked up by each unit

of XX. To find the total cost of a unit of XX the direct costs must be added on.

102