Page 143 - Microsoft Word - 00 ACCA F2 Prelims.docx

P. 143

Process costing

Process costing

Process costing is the costing method applicable where goods or

services result from a sequence of continuous or repetitive operations

or processes.

Process costing is used when a company is mass producing the same item and the

item goes through a number of different stages.

Process costing is an example of continuous operation costing.

Examples include the chemical, cement, oil refinery, paint and textile industries.

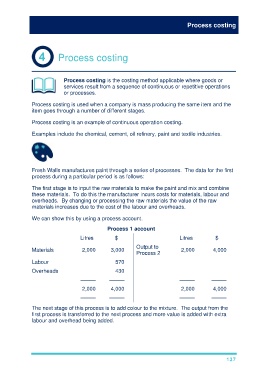

Fresh Walls manufactures paint through a series of processes. The data for the first

process during a particular period is as follows:

The first stage is to input the raw materials to make the paint and mix and combine

these materials. To do this the manufacturer incurs costs for materials, labour and

overheads. By changing or processing the raw materials the value of the raw

materials increases due to the cost of the labour and overheads.

We can show this by using a process account.

Process 1 account

Litres $ Litres $

Output to

Materials 2,000 3,000 2,000 4,000

Process 2

Labour 570

Overheads 430

––––– ––––– ––––– –––––

2,000 4,000 2,000 4,000

––––– ––––– ––––– –––––

The next stage of this process is to add colour to the mixture. The output from the

first process is transferred to the next process and more value is added with extra

labour and overhead being added.

137