Page 148 - Microsoft Word - 00 ACCA F2 Prelims.docx

P. 148

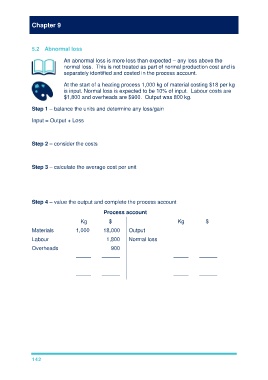

Chapter 9

5.2 Abnormal loss

An abnormal loss is more loss than expected – any loss above the

normal loss. This is not treated as part of normal production cost and is

separately identified and costed in the process account.

At the start of a heating process 1,000 kg of material costing $18 per kg

is input. Normal loss is expected to be 10% of input. Labour costs are

$1,800 and overheads are $900. Output was 800 kg.

Step 1 – balance the units and determine any loss/gain

Input = Output + Loss

1,000kg = 800kg + 100kg (NL) + 100kg (AL)

Step 2 – consider the costs

$18,000 + $1,800 + $900 = $20,700. (NL has no value)

Step 3 – calculate the average cost per unit

The cost per unit = net cost of inputs ÷ expected output

The cost per unit = $20,700 ÷ (1,000kg × 90%) = $23 per unit

Step 4 – value the output and complete the process account

Process account

Kg $ Kg $

Materials 1,000 18,000 Output 800 18,400

Labour 1,800 Normal loss 100 0

Overheads 900 Abnormal loss 100 2,300

––––– –––––– ––––– ––––––

1,000 20,700 1,000 20,700

––––– –––––– ––––– ––––––

142