Page 150 - Microsoft Word - 00 ACCA F2 Prelims.docx

P. 150

Chapter 9

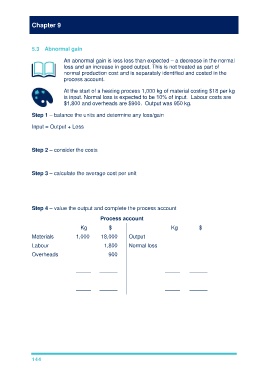

5.3 Abnormal gain

An abnormal gain is less loss than expected – a decrease in the normal

loss and an increase in good output. This is not treated as part of

normal production cost and is separately identified and costed in the

process account.

At the start of a heating process 1,000 kg of material costing $18 per kg

is input. Normal loss is expected to be 10% of input. Labour costs are

$1,800 and overheads are $900. Output was 950 kg.

Step 1 – balance the units and determine any loss/gain

Input = Output + Loss

1,000kg + 50(AG) = 950 + 100 NL

Step 2 – consider the costs

$18,000 + $1,800 + $900 = $20,700 (NL has no value)

Step 3 – calculate the average cost per unit

The cost per unit = net cost of inputs ÷ expected output

The cost per unit = $20,700 ÷ (1,000kg × 90%) = $23 per unit

Step 4 – value the output and complete the process account

Process account

Kg $ Kg $

Materials 1,000 18,000 Output 950 21,850

Labour 1,800 Normal loss 100 0

Overheads 900

Abnormal gain 50 1,150

––––– –––––– ––––– ––––––

1,050 21,850 1,050 21,850

––––– –––––– ––––– ––––––

144