Page 58 - Microsoft Word - 00 ACCA F2 Prelims.docx

P. 58

Chapter 4

Identifying cost behaviour

Understanding costs and cost behaviour is important. Managers must be

able to identify if costs are fixed, variable, stepped or semi-variable. If this

cost behaviour is understood then managers are able to estimate or

predict costs going forward.

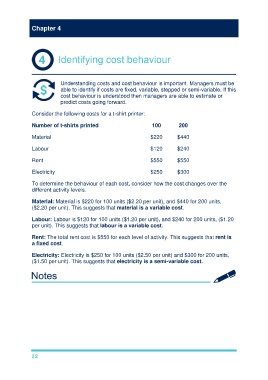

Consider the following costs for a t-shirt printer:

Number of t-shirts printed 100 200

Material $220 $440

Labour $120 $240

Rent $550 $550

Electricity $250 $300

To determine the behaviour of each cost, consider how the cost changes over the

different activity levels.

Material: Material is $220 for 100 units ($2.20 per unit), and $440 for 200 units,

($2.20 per unit). This suggests that material is a variable cost.

Labour: Labour is $120 for 100 units ($1.20 per unit), and $240 for 200 units, ($1.20

per unit). This suggests that labour is a variable cost.

Rent: The total rent cost is $550 for each level of activity. This suggests that rent is

a fixed cost.

Electricity: Electricity is $250 for 100 units ($2.50 per unit) and $300 for 200 units,

($1.50 per unit). This suggests that electricity is a semi-variable cost.

52