Page 11 - PowerPoint Presentation

P. 11

COST VOLUME PROFIT ANALYSIS

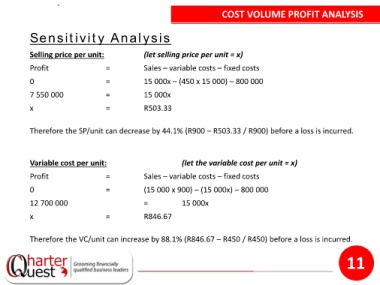

Sensitivity Analysis

Selling price per unit: (let selling price per unit = x)

Profit = Sales – variable costs – fixed costs

0 = 15 000x – (450 x 15 000) – 800 000

7 550 000 = 15 000x

x = R503.33

Therefore the SP/unit can decrease by 44.1% (R900 – R503.33 / R900) before a loss is incurred.

Variable cost per unit: (let the variable cost per unit = x)

Profit = Sales – variable costs – fixed costs

0 = (15 000 x 900) – (15 000x) – 800 000

12 700 000 = 15 000x

x = R846.67

Therefore the VC/unit can increase by 88.1% (R846.67 – R450 / R450) before a loss is incurred.

11