Page 3 - PowerPoint Presentation

P. 3

COST VOLUME PROFIT ANALYSIS

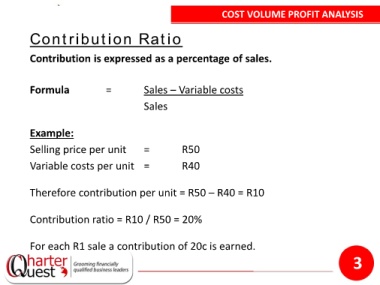

Contribution Ratio

Contribution is expressed as a percentage of sales.

Formula = Sales – Variable costs

Sales

Example:

Selling price per unit = R50

Variable costs per unit = R40

Therefore contribution per unit = R50 – R40 = R10

Contribution ratio = R10 / R50 = 20%

For each R1 sale a contribution of 20c is earned.

3