Page 34 - FINAL CFA II SLIDES JUNE 2019 DAY 7

P. 34

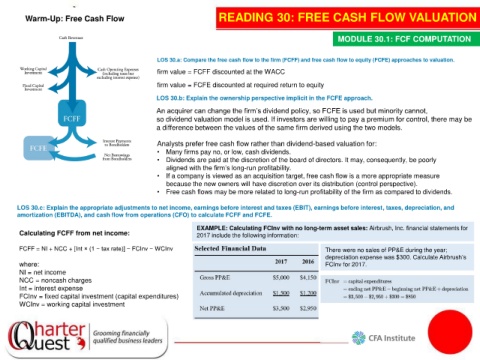

Warm-Up: Free Cash Flow READING 30: FREE CASH FLOW VALUATION

MODULE 30.1: FCF COMPUTATION

LOS 30.a: Compare the free cash flow to the firm (FCFF) and free cash flow to equity (FCFE) approaches to valuation.

firm value = FCFF discounted at the WACC

firm value = FCFE discounted at required return to equity

LOS 30.b: Explain the ownership perspective implicit in the FCFE approach.

An acquirer can change the firm’s dividend policy, so FCFE is used but minority cannot,

so dividend valuation model is used. If investors are willing to pay a premium for control, there may be

a difference between the values of the same firm derived using the two models.

Analysts prefer free cash flow rather than dividend-based valuation for:

• Many firms pay no, or low, cash dividends.

• Dividends are paid at the discretion of the board of directors. It may, consequently, be poorly

aligned with the firm’s long-run profitability.

• If a company is viewed as an acquisition target, free cash flow is a more appropriate measure

because the new owners will have discretion over its distribution (control perspective).

• Free cash flows may be more related to long-run profitability of the firm as compared to dividends.

LOS 30.c: Explain the appropriate adjustments to net income, earnings before interest and taxes (EBIT), earnings before interest, taxes, depreciation, and

amortization (EBITDA), and cash flow from operations (CFO) to calculate FCFF and FCFE.

EXAMPLE: Calculating FCInv with no long-term asset sales: Airbrush, Inc. financial statements for

Calculating FCFF from net income: 2017 include the following information:

FCFF = NI + NCC + [Int × (1 − tax rate)] − FCInv − WCInv There were no sales of PP&E during the year;

depreciation expense was $300. Calculate Airbrush’s

where: FCInv for 2017.

NI = net income

NCC = noncash charges

Int = interest expense

FCInv = fixed capital investment (capital expenditures)

WCInv = working capital investment