Page 21 - PowerPoint Presentation

P. 21

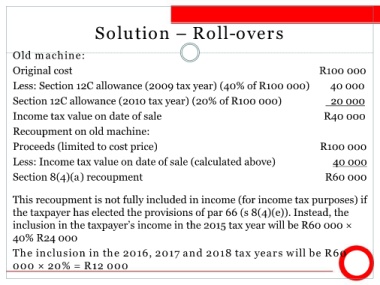

Solution – Roll-overs

Old machine:

Original cost R100 000

Less: Section 12C allowance (2009 tax year) (40% of R100 000) 40 000

Section 12C allowance (2010 tax year) (20% of R100 000) 20 000

Income tax value on date of sale R40 000

Recoupment on old machine:

Proceeds (limited to cost price) R100 000

Less: Income tax value on date of sale (calculated above) 40 000

Section 8(4)(a) recoupment R60 000

This recoupment is not fully included in income (for income tax purposes) if

the taxpayer has elected the provisions of par 66 (s 8(4)(e)). Instead, the

inclusion in the taxpayer’s income in the 2015 tax year will be R60 000 ×

40% R24 000

The inclusion in the 2016, 2017 and 2018 tax years will be R60

000 × 20% = R12 000