Page 22 - PowerPoint Presentation

P. 22

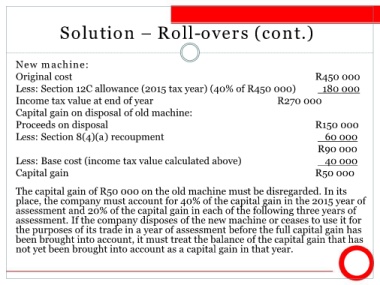

Solution – Roll-overs (cont.)

New machine:

Original cost R450 000

Less: Section 12C allowance (2015 tax year) (40% of R450 000) 180 000

Income tax value at end of year R270 000

Capital gain on disposal of old machine:

Proceeds on disposal R150 000

Less: Section 8(4)(a) recoupment 60 000

R90 000

Less: Base cost (income tax value calculated above) 40 000

Capital gain R50 000

The capital gain of R50 000 on the old machine must be disregarded. In its

place, the company must account for 40% of the capital gain in the 2015 year of

assessment and 20% of the capital gain in each of the following three years of

assessment. If the company disposes of the new machine or ceases to use it for

the purposes of its trade in a year of assessment before the full capital gain has

been brought into account, it must treat the balance of the capital gain that has

not yet been brought into account as a capital gain in that year.