Page 499 - Microsoft Word - 00 CIMA F1 Prelims STUDENT 2018.docx

P. 499

Answers

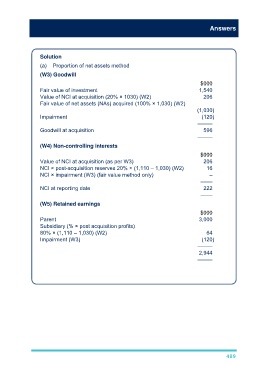

Solution

(a) Proportion of net assets method

(W3) Goodwill

$000

Fair value of investment 1,540

Value of NCI at acquisition (20% × 1030) (W2) 206

Fair value of net assets (NAs) acquired (100% × 1,030) (W2)

(1,030)

Impairment (120)

–––––

Goodwill at acquisition 596

–––––

(W4) Non-controlling interests

$000

Value of NCI at acquisition (as per W3) 206

NCI × post-acquisition reserves 20% × (1,110 – 1,030) (W2) 16

NCI × impairment (W3) (fair value method only) –

––––

NCI at reporting date 222

––––

(W5) Retained earnings

$000

Parent 3,000

Subsidiary (% × post acquisition profits)

80% × (1,110 – 1,030) (W2) 64

Impairment (W3) (120)

–––––

2,944

–––––

489