Page 454 - F2 Integrated Workbook STUDENT 2019

P. 454

Chapter 19

Chapter 11

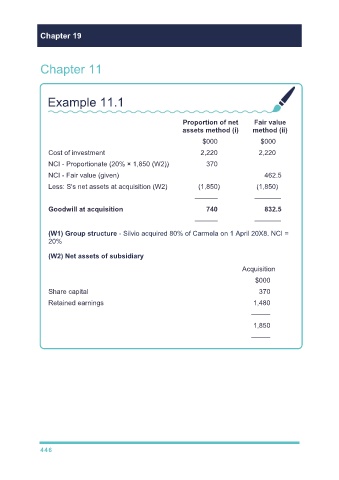

Example 11.1

Proportion of net Fair value

assets method (i) method (ii)

$000 $000

Cost of investment 2,220 2,220

NCI - Proportionate (20% × 1,850 (W2)) 370

NCI - Fair value (given) 462.5

Less: S's net assets at acquisition (W2) (1,850) (1,850)

–––––– –––––––

Goodwill at acquisition 740 832.5

–––––– –––––––

(W1) Group structure - Silvio acquired 80% of Carmela on 1 April 20X8. NCI =

20%

(W2) Net assets of subsidiary

Acquisition

$000

Share capital 370

Retained earnings 1,480

–––––

1,850

–––––

446