Page 187 - F3 -FA Integrated Workbook STUDENT 2018-19

P. 187

Capital structure and finance costs

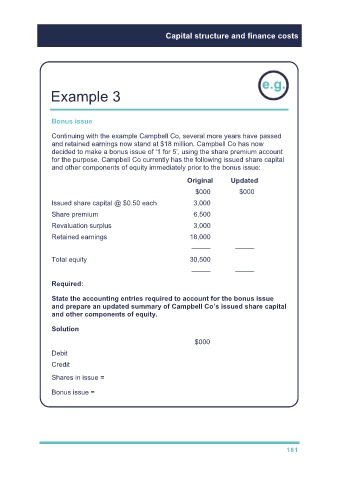

Example 3

Bonus issue

Continuing with the example Campbell Co, several more years have passed

and retained earnings now stand at $18 million. Campbell Co has now

decided to make a bonus issue of ‘1 for 5’, using the share premium account

for the purpose. Campbell Co currently has the following issued share capital

and other components of equity immediately prior to the bonus issue:

Original Updated

$000 $000

Issued share capital @ $0.50 each 3,000 3,600

Share premium 6,500 5,900

Revaluation surplus 3,000 3,000

Retained earnings 18,000 18,000

––––– –––––

Total equity 30,500 30,500

––––– –––––

Required:

State the accounting entries required to account for the bonus issue

and prepare an updated summary of Campbell Co’s issued share capital

and other components of equity.

Solution

$000

Debit Share premium 600

Credit Equity share capital @ $0.5 each 600

Shares in issue = 3m × 2 = 6m

Bonus issue = 6m/5 = 1.2m shares issued @ $0.5 nominal value each

181