Page 316 - F3 -FA Integrated Workbook STUDENT 2018-19

P. 316

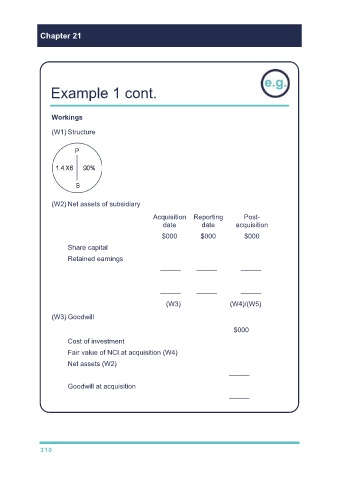

Chapter 21

Example 1 cont.

Workings

(W1) Structure

Note: NCI = 10%

(W2) Net assets of subsidiary

Acquisition Reporting Post-

date date acquisition

$000 $000 $000

Share capital 10,000 10,000

Retained earnings 3,000 4,200 1,200

——— ——— ———

13,000 14,200 1,200

——— ——— ———

(W3) (W4)/(W5)

(W3) Goodwill

$000

Cost of investment 19,000

Fair value of NCI at acquisition (W4) 2,000

Net assets (W2) (13,000)

———

Goodwill at acquisition 8,000

———

310