Page 326 - F3 -FA Integrated Workbook STUDENT 2018-19

P. 326

Chapter 21

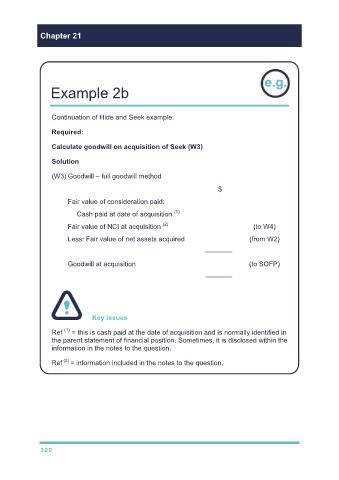

Example 2b

Continuation of Hide and Seek example:

Required:

Calculate goodwill on acquisition of Seek (W3)

Solution

(W3) Goodwill – full goodwill method

$

Fair value of consideration paid:

(1)

Cash paid at date of acquisition 300,000

(2)

Fair value of NCI at acquisition 50,000 (to W4)

Less: Fair value of net assets acquired (211,000) (from W2)

–––––––

Goodwill at acquisition (to SOFP)

–––––––

Key issues

(1)

Ref = this is cash paid at the date of acquisition and is normally identified in

the parent statement of financial position. Sometimes, it is disclosed within the

information in the notes to the question.

Ref (2) = information included in the notes to the question.

320