Page 288 - PM Integrated Workbook 2018-19

P. 288

Chapter 10

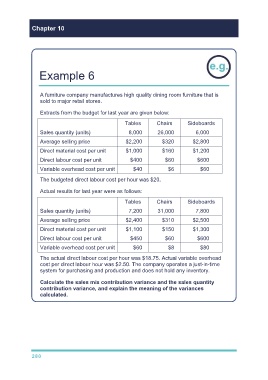

Example 6

A furniture company manufactures high quality dining room furniture that is

sold to major retail stores.

Extracts from the budget for last year are given below:

Tables Chairs Sideboards

Sales quantity (units) 8,000 26,000 6,000

Average selling price $2,200 $320 $2,800

Direct material cost per unit $1,000 $160 $1,200

Direct labour cost per unit $400 $60 $600

Variable overhead cost per unit $40 $6 $60

The budgeted direct labour cost per hour was $20.

Actual results for last year were as follows:

Tables Chairs Sideboards

Sales quantity (units) 7,200 31,000 7,800

Average selling price $2,400 $310 $2,500

Direct material cost per unit $1,100 $150 $1,300

Direct labour cost per unit $450 $60 $600

Variable overhead cost per unit $60 $8 $80

The actual direct labour cost per hour was $18.75. Actual variable overhead

cost per direct labour hour was $2.50. The company operates a just-in-time

system for purchasing and production and does not hold any inventory.

Calculate the sales mix contribution variance and the sales quantity

contribution variance, and explain the meaning of the variances

calculated.

280