Page 386 - PM Integrated Workbook 2018-19

P. 386

Chapter 15

Chapter 4

Example 1

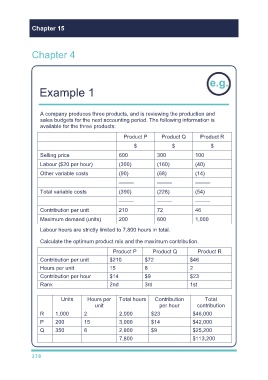

A company produces three products, and is reviewing the production and

sales budgets for the next accounting period. The following information is

available for the three products:

Product P Product Q Product R

$ $ $

Selling price 600 300 100

Labour ($20 per hour) (300) (160) (40)

Other variable costs (90) (68) (14)

––––– ––––– –––––

Total variable costs (390) (228) (54)

––––– ––––– –––––

Contribution per unit 210 72 46

Maximum demand (units) 200 600 1,000

Labour hours are strictly limited to 7,800 hours in total.

Calculate the optimum product mix and the maximum contribution.

Product P Product Q Product R

Contribution per unit $210 $72 $46

Hours per unit 15 8 2

Contribution per hour $14 $9 $23

Rank 2nd 3rd 1st

Units Hours per Total hours Contribution Total

unit per hour contribution

R 1,000 2 2,000 $23 $46,000

P 200 15 3,000 $14 $42,000

Q 350 8 2,800 $9 $25,200

7,800 $113,200

378