Page 269 - Microsoft Word - 00 Prelims.docx

P. 269

Divisional performance measurement and transfer pricing

Divisional performance measurement

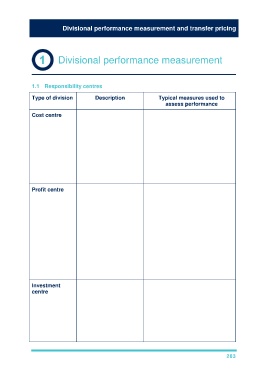

1.1 Responsibility centres

Type of division Description Typical measures used to

assess performance

Cost centre Division incurs costs Unexpected price decrease

but has no revenue due to:

stream, e.g. the IT

support department – Lower than anticipated

of an organisation customer demand

– Higher than anticipated

demand for competitor’s

products

– A reduction in quality or

performance

Profit centre Division has both All of the above PLUS:

costs and revenue

– Total sales and market

Manager does not share

have the authority to

alter the level of – Profit

investment in the – Sales variances

division

– Working capital ratios

(depending on the

division concerned)

– NFPIs e.g. related to

productivity, quality and

customer satisfaction

Investment Division has both All of the above PLUS:

centre costs and revenue

– ROI

Manager does have

the authority to – RI

invest in new assets These measures are used to assess

or dispose of the investment decisions made by

existing ones

managers and are discussed in

more detail below

263