Page 66 - Microsoft Word - 00 Prelims.docx

P. 66

Chapter 3

Single product breakeven analysis

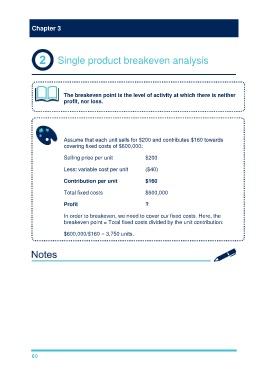

The breakeven point is the level of activity at which there is neither

profit, nor loss.

Assume that each unit sells for $200 and contributes $160 towards

covering fixed costs of $600,000:

Selling price per unit $200

Less: variable cost per unit ($40)

Contribution per unit $160

Total fixed costs $600,000

Profit ?

In order to breakeven, we need to cover our fixed costs. Here, the

breakeven point = Total fixed costs divided by the unit contribution:

$600,000/$160 = 3,750 units.

60