Page 49 - MAC4861_2 Costing Class Slides Part 1

P. 49

TEST 3 - COSTING

Costing variances – example 1

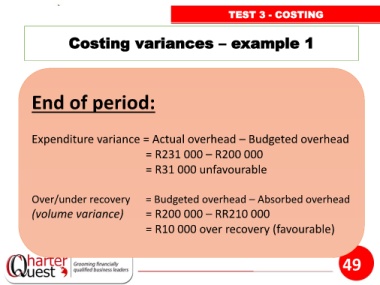

End of period:

Expenditure variance = Actual overhead – Budgeted overhead

= R231 000 – R200 000

= R31 000 unfavourable

Over/under recovery = Budgeted overhead – Absorbed overhead

(volume variance) = R200 000 – RR210 000

= R10 000 over recovery (favourable)

49