Page 46 - MAC4861_2 Costing Class Slides Part 1

P. 46

TEST 3 - COSTING

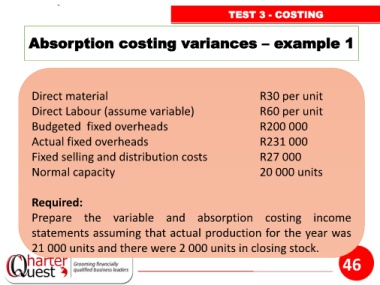

Absorption costing variances – example 1

Direct material R30 per unit

Direct Labour (assume variable) R60 per unit

Budgeted fixed overheads R200 000

Actual fixed overheads R231 000

Fixed selling and distribution costs R27 000

Normal capacity 20 000 units

Required:

Prepare the variable and absorption costing income

statements assuming that actual production for the year was

21 000 units and there were 2 000 units in closing stock.

46